VC due diligence at seed stage is a proof problem. Investors repeat the same questions across every meeting because they need to determine what is real: the team, the traction, the market. Founders who arrive with proof already built close faster because investors can confirm what is real before the first call starts.

This guide covers what seed diligence actually looks like, why the process repeats, and how structured proof breaks the loop.

Seed Stage Due Diligence Is Not What Most Founders Expect

Most founders picture due diligence as a formal audit. Lawyers reviewing contracts. Analysts building financial models. That is Series A and later. At seed stage, diligence looks different.

A typical seed investor will run a few customer calls, glance at the cap table, check for obvious IP issues, and call references through their own network. Much of the formal legal and financial review happens after the term sheet is signed, not before. Competitive markets forced this shift: doing full diligence before a term sheet in a fast round is too slow.

So what happens before the term sheet? Conversations. A lot of them.

According to DocSend's 2023 seed fundraising research, the average seed founding team has 38 investor meetings before closing their round. The average VC spends just 2 minutes and 24 seconds reviewing a pitch deck (DocSend, 2024). That is not enough time to understand whether a startup is real. So they schedule a call. Then another. Then another.

These are not informational meetings. They are proof mechanisms. Each question tests a specific claim: is the team capable, is the traction genuine, is the market large enough, is the plan realistic. The investor is not curious. The investor is trying to determine what is true.

Research surveying 885 institutional venture capitalists at 681 firms found that the management team was rated the most important investment factor by 95% of VCs, and the single most important factor by 47% (Gompers et al., Journal of Financial Economics, 2020). More than market size, product, or technology. Every early meeting is built around this question: can this team be trusted to execute?

Why Paper Cannot Prove What Investors Need to Know

Decks are curated. Every word is chosen to make the startup look its best. Financial models are built on assumptions the founder selected. Market sizing numbers are pulled from analyst reports. Competitive analyses omit the most dangerous competitors. None of this tells an investor what is real.

This is why investors do not trust documents alone. They need to see how a founder thinks. They ask a question the founder has not prepared for and watch what happens. They push on a weak point and see whether the founder defends a losing position or updates their view. This is how conviction forms. Not from slides. From live proof that the founder knows their business at a level deeper than the pitch.

Only 30% of VCs use quantitative financial models during due diligence (Gompers et al., 2020). The rest rely on qualitative judgment formed through conversation. The average VC reviews 101 opportunities for every single deal they fund. That is 101 startups competing for one check, and the deciding factor is almost never the deck. It is whether the investor believes the founder's claims are real.

I spent 7 years on the investor side leading diligence. Some founders came in with well-organized Notion pages covering product, team, financials, everything we needed to understand on paper. Those were a green flag. They made our job easier, which was good for the startup. But a well-structured data room was never the deciding factor. Paper can be polished. It always came down to the person: how they answered when we asked questions live, whether they could go deeper than the prepared material. The founders who held their ground under pressure, admitted what they did not know, and pointed to real evidence instead of assertions were the ones who earned second meetings. Documents got them in the door. Proof got them funded.

The Repetition Trap: Every Investor Starts From Zero

Here is the part nobody warns you about before you start fundraising.

When you finish a meeting with Fund A on Monday and pitch Fund B on Tuesday, Fund B has no idea what happened with Fund A. They have not read Fund A's notes. They have not seen which questions were already answered in depth. They start fresh. Every time.

This is not laziness. It comes down to competitive dynamics. When two or three funds are competing for the lead position in your round, they share nothing with each other. All they will say publicly is "yeah, we are looking at this deal." However, when a lead investor is already in place and a smaller check or a strategic co-investor is considering the round, some diligence findings do get shared. And investors talk extensively about deals they pass on, sharing what they found and why they walked away. The practical result: the investors whose conviction you need most are the ones doing their own work from scratch. That conviction cannot be transferred.

The result is brutal repetition. You explain your founding story to 15 different partners. You walk through the same market sizing logic in 20 separate conversations. You answer "what are your unit economics?" the same way each time.

Here is the frustrating part: those questions are not bad questions. From the investor side, the pre-decision diligence is focused. It zeroes in on the things that could kill the deal or confirm the thesis: team, market, traction, red flags. The tedious operational work, cap table review, legal checks, follow-ups on minor issues, that all happens after the fund has already decided it wants to invest. It is mostly process, and it rarely changes the outcome. The bottleneck is not that investors ask pointless questions. The bottleneck is that 15 different investors each need to ask the same pointed questions because none of them can inherit another fund's conviction.

The average seed founder spends more than 6 months fundraising and repeats the same answers across 15 to 20 investor meetings (Crunchbase, 2025). Carta's 2025 data shows the median seed round now takes 142 days to close, up from 69 days in 2021. Forum Ventures analyzed 300+ B2B SaaS pre-seed and seed deals from 2024 and found that raise cycles now run 12 to 18 months for most founders, but only 3 to 6 weeks for the top companies.

That gap is not about pitch quality. It is about proof. The top companies arrive with evidence that answers the diligence questions before the questions get asked. Everyone else grinds through the loop.

The reason the same questions recur is structural. A 2023 systematic review of venture capital funding identified information asymmetry between founder and investor as the core inefficiency: uncertainty is what creates VC returns, but it also forces every fund to rebuild its own information map from scratch (ScienceDirect, Inefficiencies of Venture Capital Funding, 2023). A 2022 meta-analysis of VC signal use found that the signals investors rely on are imperfect predictors of actual outcomes, which is exactly why live questioning persists (ScienceDirect, Information Signals and Bias in VC, 2022). The loop is not about you. It is about a system where every fund is building conviction alone, using signals that nobody trusts completely.

Why Cutting Diligence Hurts Everyone

Founders might think that less diligence means faster closes. The data says the opposite.

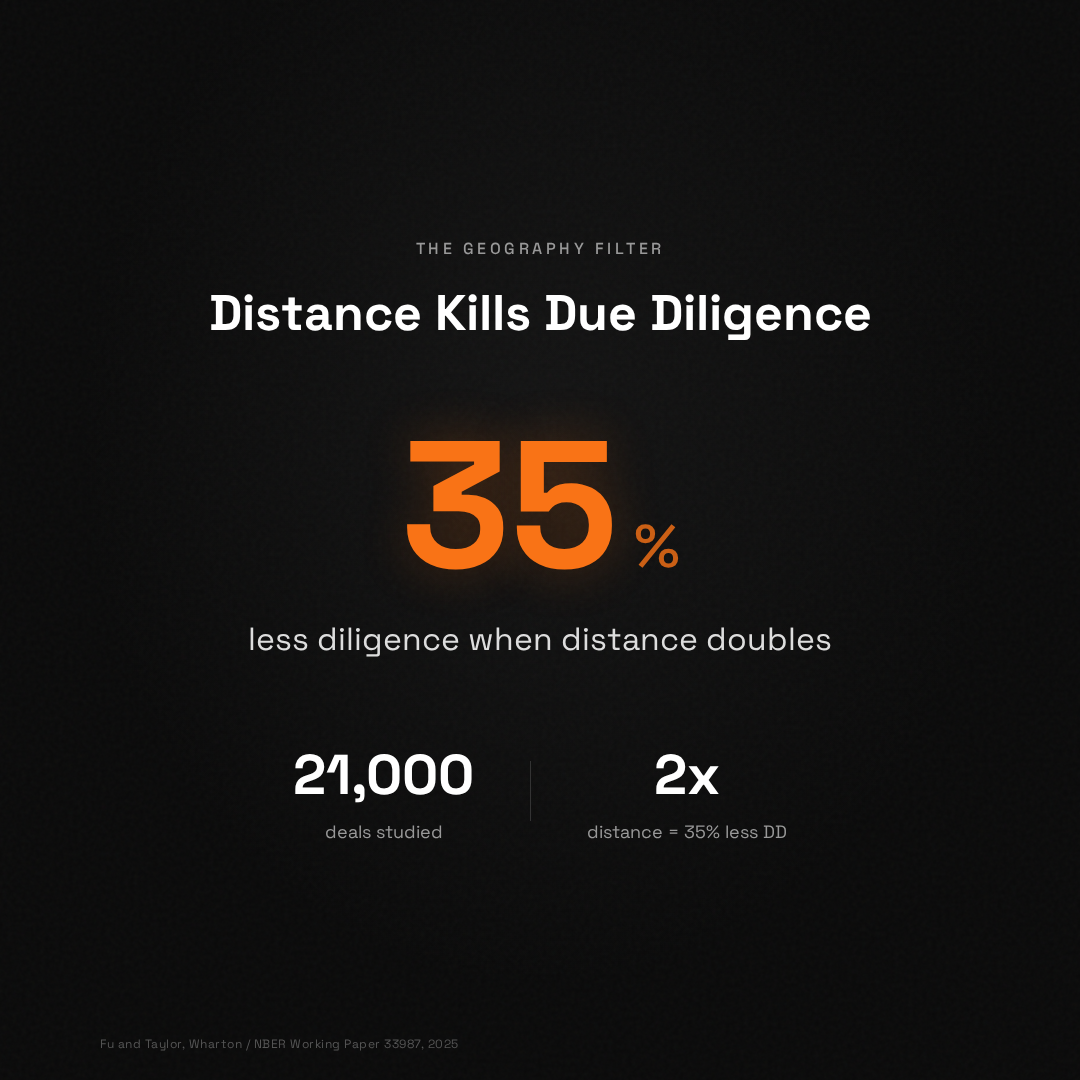

Research by Xiaoyong Fu and Lucian Taylor of the Wharton School studied 21,000 venture capital deals using cell phone signal data to measure the actual duration of meetings between VCs and founders (Fu and Taylor, NBER Working Paper 33987, 2025). Their findings are striking. 95% of deals showed zero detected in-person due diligence. When VCs did perform diligence, they spent an average of 32 hours on it. But diligence dropped by 35% when geographic distance doubled, by 13% when competing VCs were present, and by 22% when the VC firm was busy with its existing portfolio.

Less diligence correlated with more volatile outcomes. Both better and worse. The uncertainty increased because proof was never established.

This matters for founders in a counterintuitive way. The problem is not that investors are too rigorous. The problem is that the current process makes rigor expensive. Each fund has to build conviction from scratch through live meetings. So when time is short or competition is fierce, they skip the work entirely and rely on pattern matching instead.

The founders who lose in this system are the ones who have real businesses but no way to prove it at scale. The deck does not prove it. The meeting helps, but only one investor at a time. The proof needs to exist in a format that every investor can access independently.

The Proof Layer: What Structured Proof Looks Like

Founders who close in the first quartile of their cohort do something different. They pre-build the proof layer so the early meetings skip orientation and start at a deeper level of conviction. A 2025 review of due diligence as a legally significant, increasingly structured process argues that codifying what gets checked (team, traction, market, unit economics) is what lets diligence move from reactive to proactive (Aran & Packin, Due Diligence Dilemma, Illinois Law Review, 2025). Founders who front-load that structure do not shorten diligence; they collapse the orientation phase.

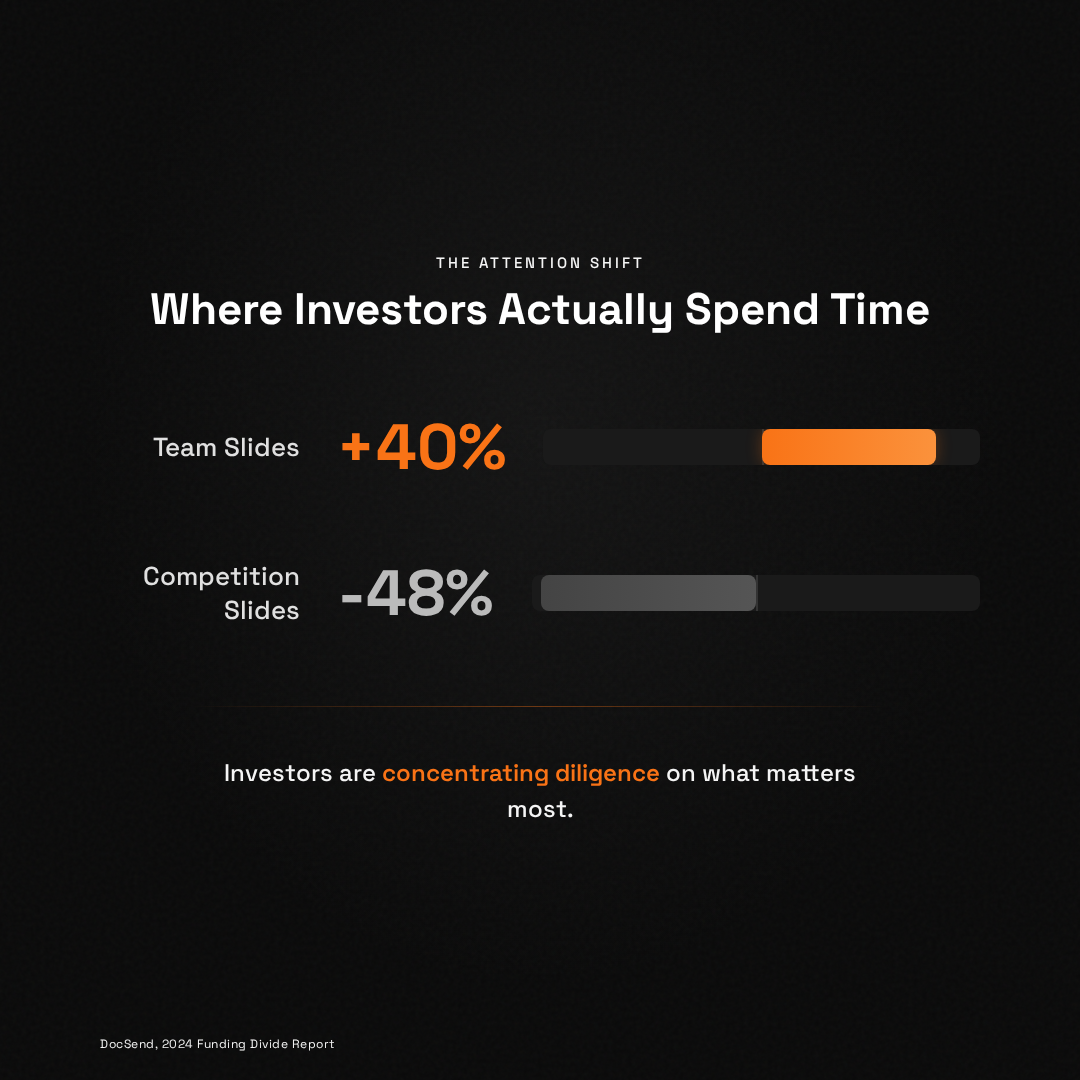

The shift on the investor side reinforces this. PitchBook-NVCA data for 2025 shows that AI and machine learning deals captured 65.6% of all US VC deal value, up from 47.2% a year earlier (PitchBook-NVCA Venture Monitor, 2025). Funds now triage the narrowest thesis in decades against the highest inbound volume in decades. That pairing rewards founders whose materials are already structured, machine-readable, and pre-answered. Diligence is not being skipped. It is being filtered and front-loaded.

Here is the difference. "We have strong traction" is a claim. "Here is our Stripe data showing $14K MRR growing 22% month over month, connected live" is proof. "Our team is strong" is a claim. "Here is a structured breakdown of each founder's domain expertise, with the specific questions that tested their depth" is proof.

The shift from claim to proof is what separates a 6 month fundraise from a 6 week fundraise. Not a better pitch. Better evidence.

SeedForge was built to close the gap between your data room and your first live meeting. One 30-minute AI session stress-tests the same questions investors will ask, so you walk in knowing where you are strong and where you will get pushed. The output is a Living Profile: structured answers, real traction data connected via API, and documents in one shareable link. It does not replace the conversation. It makes the conversation start at the right level. Whether you are raising now or six months from now, the session shows you exactly where your proof stands. Start free at seedforge.com.

The market is moving this direction. Research on AI adoption in VC shows that 85% of private capital dealmakers now use AI for daily tasks, up from 76% the prior year (Affinity, 2026). One fund reported cutting screening time from 45 minutes to 8 minutes per company. The expectation of structured, accessible proof is becoming the norm, not the exception.

Pre-Fundraise Proof Checklist: What to Have Ready Before Meeting 1

To be clear: documents do not replace live meetings. They never will. But they set the agenda. They save the investor from spending the first 15 minutes asking "what do you do?" They signal that you have thought through the business before anyone asked you to. A well-prepared data room does not build conviction on its own, but it earns you the meeting where conviction gets built.

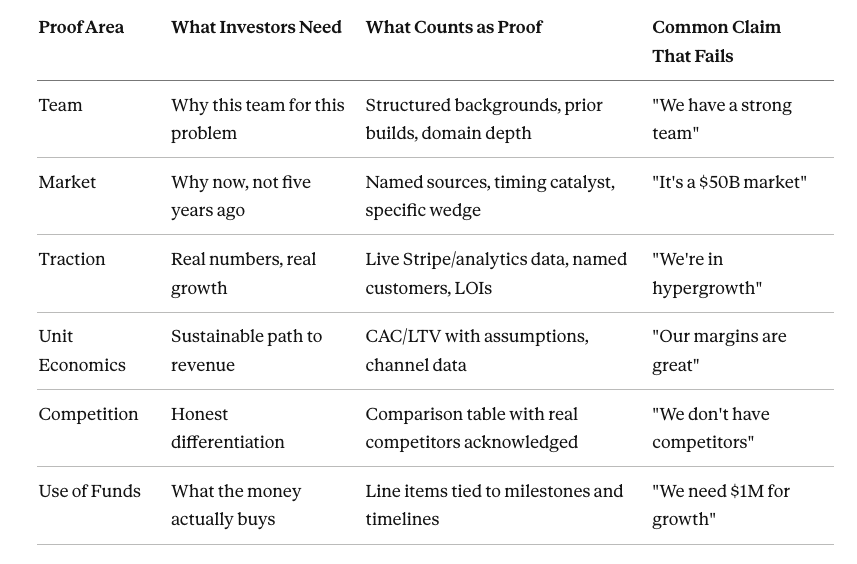

Before your first investor conversation, every claim in your pitch should have evidence behind it. Here is what to build.

Team proof. Structured backgrounds for each founder: what you built before, what domain expertise you bring, why this team for this problem. The goal is for an investor to understand team quality without reading through your entire LinkedIn history.

Market proof. Total addressable market with a named source, publication date, and sample size. Your serviceable market, sized with specifics. The specific reason this market is ready now, not five years ago. Timing proof is more valuable than size proof.

Traction proof. Real numbers connected to real sources. Monthly or annual recurring revenue with growth rate. If pre-revenue: signed LOIs, waitlist numbers, customer quotes with named companies. Whatever you have, document it with evidence, not assertions.

Unit economics proof. Customer acquisition cost and lifetime value if you have the data. If pre-revenue, your best estimate of acquisition channels and customer value with the assumptions spelled out. Honest estimates build more trust than confident projections.

Competition proof. A comparison table showing your main competitors, what they do well, and where you are different. The goal is not to dismiss competitors. It is to show honest analysis. Investors see founders handwave competitors every day. They trust founders who acknowledge them.

Use of funds proof. How much you are raising and what it buys in concrete terms. Two engineering hires and six months of runway toward a specific product milestone. Marketing spend tied to a channel with a cost per acquisition assumption. Show what the money does, not just how much you want.

Legal proof. Clean cap table. Proper incorporation. Founder vesting in place. IP assigned to the company. If there are complications, surface them early. Investors always find out eventually.

75% of VC-backed companies fail to return capital to investors (Ghosh, Harvard Business School). Investors know this. Every question they ask is an attempt to determine whether your startup will be in the 25% that works. The more proof you provide upfront, the less guessing they have to do.

The Questions That Come Up in Every First Seed Meeting

These questions will come up. The difference is whether you answer them live for the first time, or whether an investor has already seen your proof and the meeting starts one level deeper.

Why this market, and why now? Not why the market is large. Why it is ready to move in the next 24 months. A specific technological shift, regulatory change, or behavioral shift that makes the timing real.

What is your unfair advantage? Not your features. Your structural advantage. Why this team builds this, and why a well-funded competitor cannot replicate it in 18 months. The Gompers research found that 885 VCs rated team as the primary factor. Unfair advantage almost always starts with the people.

What are your real numbers? Not best-case projections. Actual current metrics. Revenue, growth rate, churn if applicable. Specificity builds trust. "$8,400 MRR growing 22% month over month" is more credible than "we're growing fast."

Who have you sold to, and what did they say? Customer evidence matters more than customer count. One customer who switched from a competitor is stronger proof than 50 free trials.

What does success look like in 18 months? The milestone your raise funds. Investors want to know what the money unlocks and what triggers the next round. A clear answer proves you have thought through the business, not just the pitch.

VCs back approximately 5 to 12 companies per year on average, reviewing hundreds of pitches to reach those decisions (NVCA, 2025). They cannot spend weeks on every company. Founders who arrive with proof make the investor's decision easier. Not by shortcutting diligence, but by establishing what is real before the meeting starts.

Frequently Asked Questions

How long does seed stage VC due diligence take?

Pre-term sheet diligence at seed stage typically runs 2 to 6 weeks from first meeting to signed term sheet. The median seed round closes in 142 days (Carta, 2025), up from 69 days in 2021. Founders who arrive with structured proof of team, traction, and market shorten this timeline because investors spend less time establishing basics and more time building conviction.

How many investor meetings does it take to close a seed round?

The average seed founding team has 38 investor meetings before closing (DocSend, 2023). This includes first meetings, follow-ups, partner meetings, and diligence calls across multiple funds. Founders who provide structured proof before the first call reduce the total meeting count because each conversation starts deeper.

What do VCs actually check in seed stage due diligence?

VCs check four areas at seed stage: the founding team (backgrounds, domain expertise, co-founder dynamics), the market (size, timing, competitive landscape), current traction (revenue, growth rate, customer evidence), and basic legal hygiene (incorporation, cap table, IP ownership). The management team is rated most important by 95% of VCs (Gompers et al., 2020). Detailed legal review usually happens post-term sheet.

What is the single most important factor in a VC investment decision?

According to a survey of 885 institutional VCs at 681 firms, the management team is the most important factor. 47% named the team as the single most important factor, above market size (2%), product (14%), and business model (37%) (Gompers et al., Journal of Financial Economics, 2020). This is why live meetings focus so heavily on the founders themselves.

How can founders stop repeating the same answers to every investor?

The repetition happens because each fund builds conviction independently. No investor reads another fund's notes. The solution is structured proof shared via a single link: answers to the core diligence questions backed by real data that every investor can access before the first call. Tools like SeedForge produce this proof layer through a 30-minute AI session.

Why do VCs ask the same questions as every other fund?

Funds compete with each other and do not share diligence. Each partner must form their own conviction about the team, market, and traction. This means every new fund starts from zero regardless of how many other meetings you have had. The questions repeat not because investors lack imagination, but because conviction is not transferable. Structured proof shared in advance is the only way to shorten this loop without skipping the substance.

About the Author

David Rakusan spent 7 years on the investor side of early-stage fundraising, leading 30+ due diligences across European and global venture funds. He holds an MBA from INSEAD and the CFA Charter. He built SeedForge because he watched the same founders get stuck in the same loop: real businesses, real traction, but no way to prove it to 20 investors without 20 separate meetings.

SeedForge runs founders through a 30-minute AI session that asks what VCs ask in the first three meetings. The output is a Living Profile: structured answers, real traction data connected via API, and documents in one shareable link. Founders prove their startup once and share it everywhere.

Start free at seedforge.com.

Sources

Gompers, P., Gornall, W., Kaplan, S., and Strebulaev, I. (2020). "How Do Venture Capitalists Make Decisions?" Journal of Financial Economics. Sample: 885 VCs at 681 firms.

Fu, X. and Taylor, L. (2025). "Due Diligence and the Allocation of Venture Capital." NBER Working Paper 33987. Sample: 21,000 deals.

DocSend (2023). "Seed Fundraising in 2023." Dropbox/DocSend annual fundraising research.

DocSend (2024). "2024 Funding Divide Report." Pitch deck engagement data.

Carta (2025). State of Private Markets reports. Median seed close: 142 days.

Forum Ventures (2024). State of the VC Market: Pre-seed and Seed. 300+ B2B SaaS deals.

Crunchbase (2025). Global VC Report.

NVCA (2025). NVCA Yearbook.

Ghosh, S. Harvard Business School. Study of 2,000+ VC-backed companies.

Affinity (2026). VC AI Tools Report.