The right VC for your startup is the one whose thesis, stage focus, and check size already match what you are building. Most founders skip this step. They pitch broadly, hope for chemistry, and learn that investor fit is a proof problem, not a volume problem.

The founders who close faster do not pitch more investors. They pitch the right ones, with proof already in hand.

The median time between funding rounds hit 744 days in Q4 2024, up from 451 days in 2021 (Carta). That is not fundraising getting harder for everyone. It is fundraising getting harder for founders who treat it as a volume game. Targeting precision is now the single biggest lever between a six-week raise and a two-year grind.

I spent 7 years on the investor side leading due diligence. The pattern was always the same. The founders who showed up with clear thesis alignment and pre-built proof closed in weeks. Everyone else ground through months of meetings that were never going to convert.

Why Pitching Broadly Fails

Most founders treat fundraising like a numbers game. Build a list of 200 investors. Send cold emails. Book as many meetings as possible. Hope that volume converts to a term sheet.

The data says otherwise.

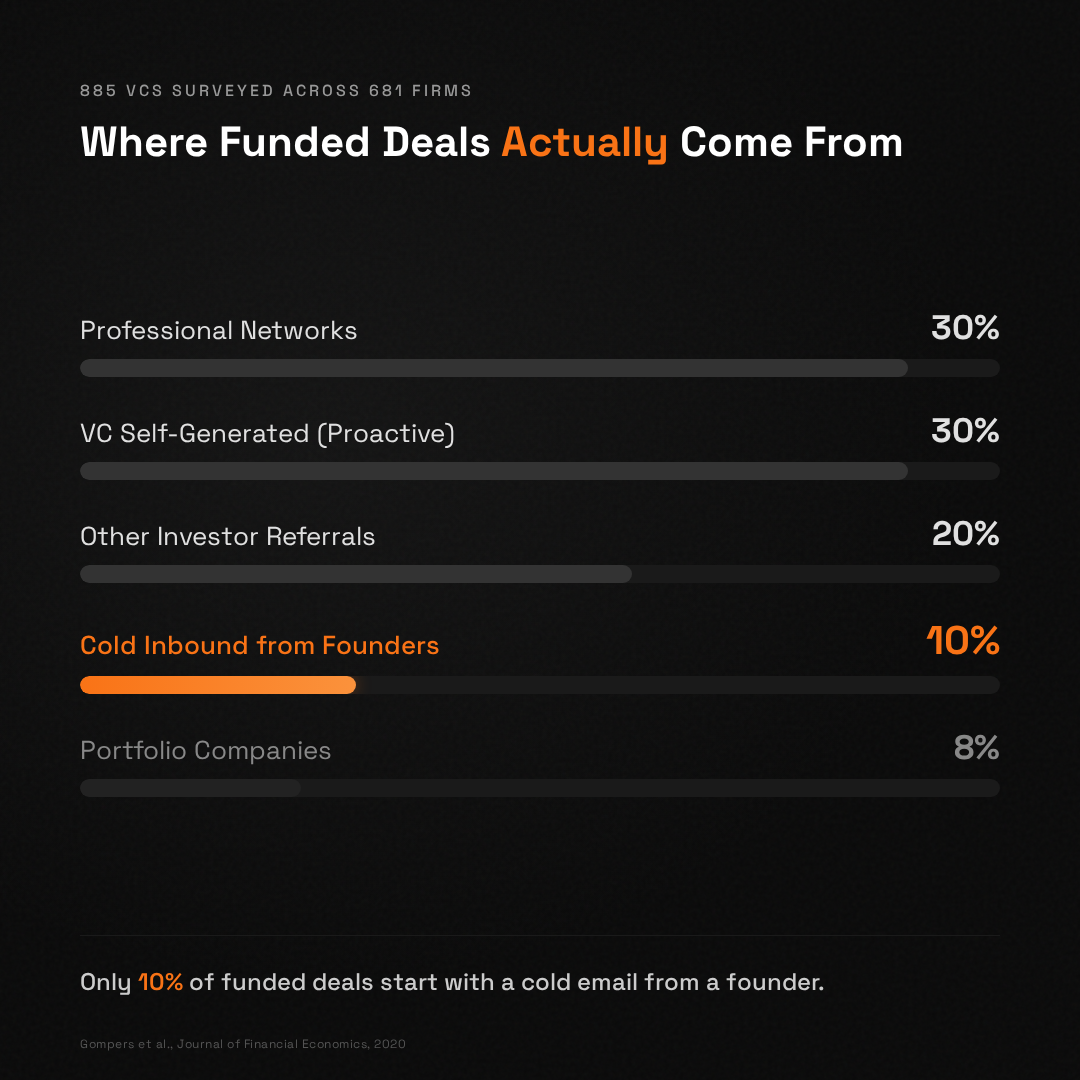

A survey of 885 institutional VCs across 681 firms mapped where funded deals actually come from (Gompers et al., Journal of Financial Economics, 2020). About 30% are sourced through professional networks. Another 30% are proactively self-generated by VCs hunting for deals. 20% come from referrals by other investors. 8% come through portfolio companies. Only 10% arrive as cold inbound from founders. Cold outreach to misaligned investors is the lowest conversion channel in venture capital.

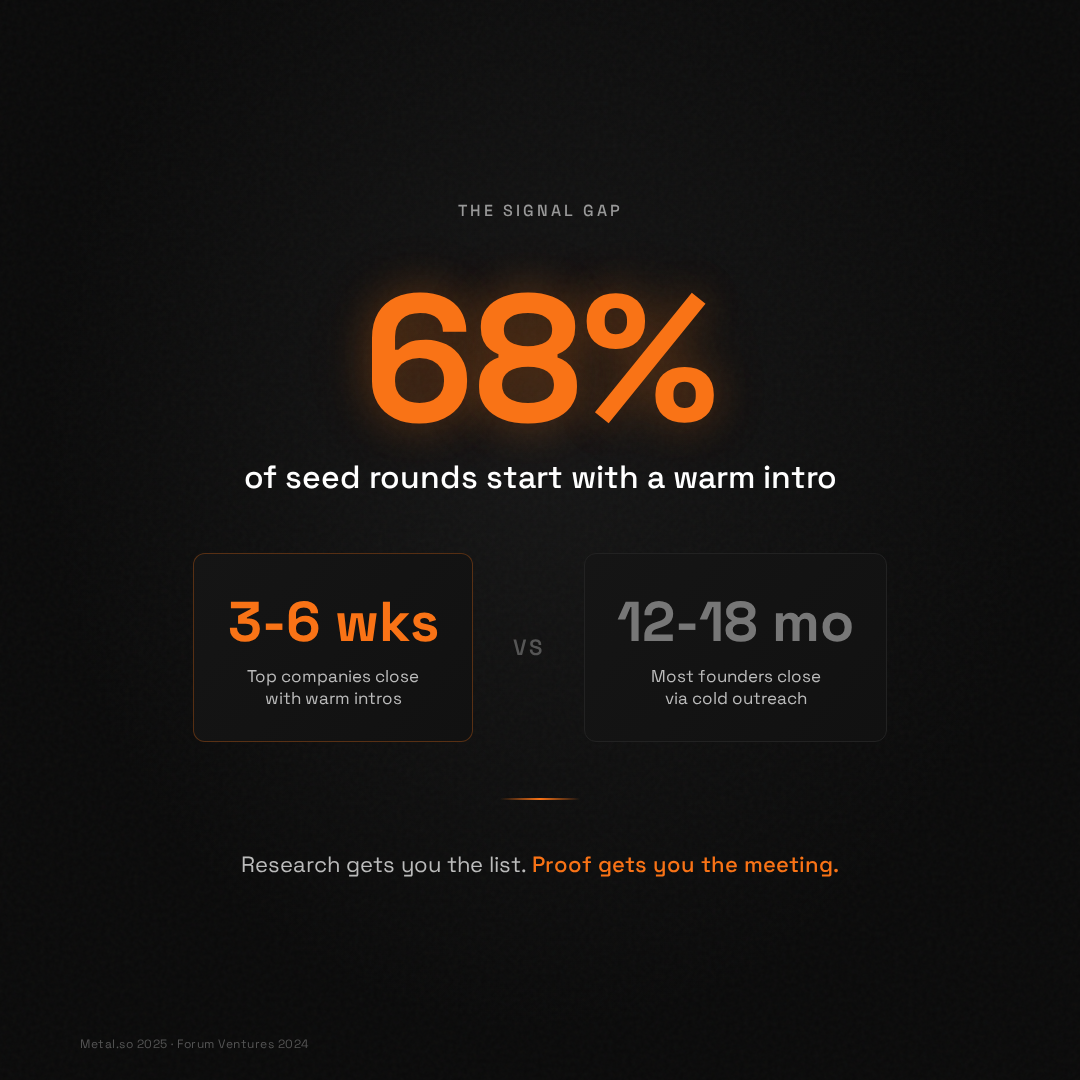

Industry data from 2025 confirms the gap. Cold email response rates for fundraising outreach sit at 1 to 5%, while warm introductions convert at dramatically higher rates (GrowLeads, Metal.so, Flowlie, 2025). About 68% of seed rounds now start with a warm introduction, up from 55% the prior year (Metal.so, 2025 Trend Analysis). Founders who blast 200 cold emails are fighting for the shrinking share of deals that close through cold channels.

Here is what that looks like from the investor side. Most thesis mismatches get sorted out while the investor is scrolling through the deck. They just pass and never reply. A clear thesis mismatch is one of the most common reasons for ghosting. But sometimes the mismatch is borderline. The investor hops on a call, realizes mid-conversation that it is not a fit, but stays on the call anyway, acts polite, maybe offers some advice, and then passes immediately after hanging up.

The investor loses 30 minutes. But the founder, unless they got a clear signal, might spend days or weeks chasing that investor with follow ups into a void. This is why thesis mismatches are so expensive. The cost is asymmetric. The investor moves on. The founder does not know they should.

Forum Ventures analyzed 300+ B2B SaaS pre-seed and seed deals from 2024 and found that fundraising cycles now run 12 to 18 months for most founders, but only 3 to 6 weeks for the top companies (Forum Ventures, 2024). The gap is not talent or product quality. It is targeting precision and pre-built proof.

What Investors Are Actually Screening For

Here is what most founders miss. VCs are not sitting in meetings trying to decide if your startup is good. They are trying to decide if your startup matches their thesis, their fund structure, and their portfolio strategy. Those are three different filters, and none of them are about you personally.

The bar for a meeting has also moved. Waveup's 2025 VC survey of 56 funds found that round expectations jumped one full stage across the board: pre-seed now expects what used to be seed traction, seed expects what used to be Series A traction (Waveup, 2025 Fundraising Study). Net Revenue Retention has emerged as a metric VCs check early. Any cold pitch that does not anticipate the new bar gets filtered out before the call. Most nos are not about quality of the startup. They are about pre-stage mismatch with the fund's current thesis.

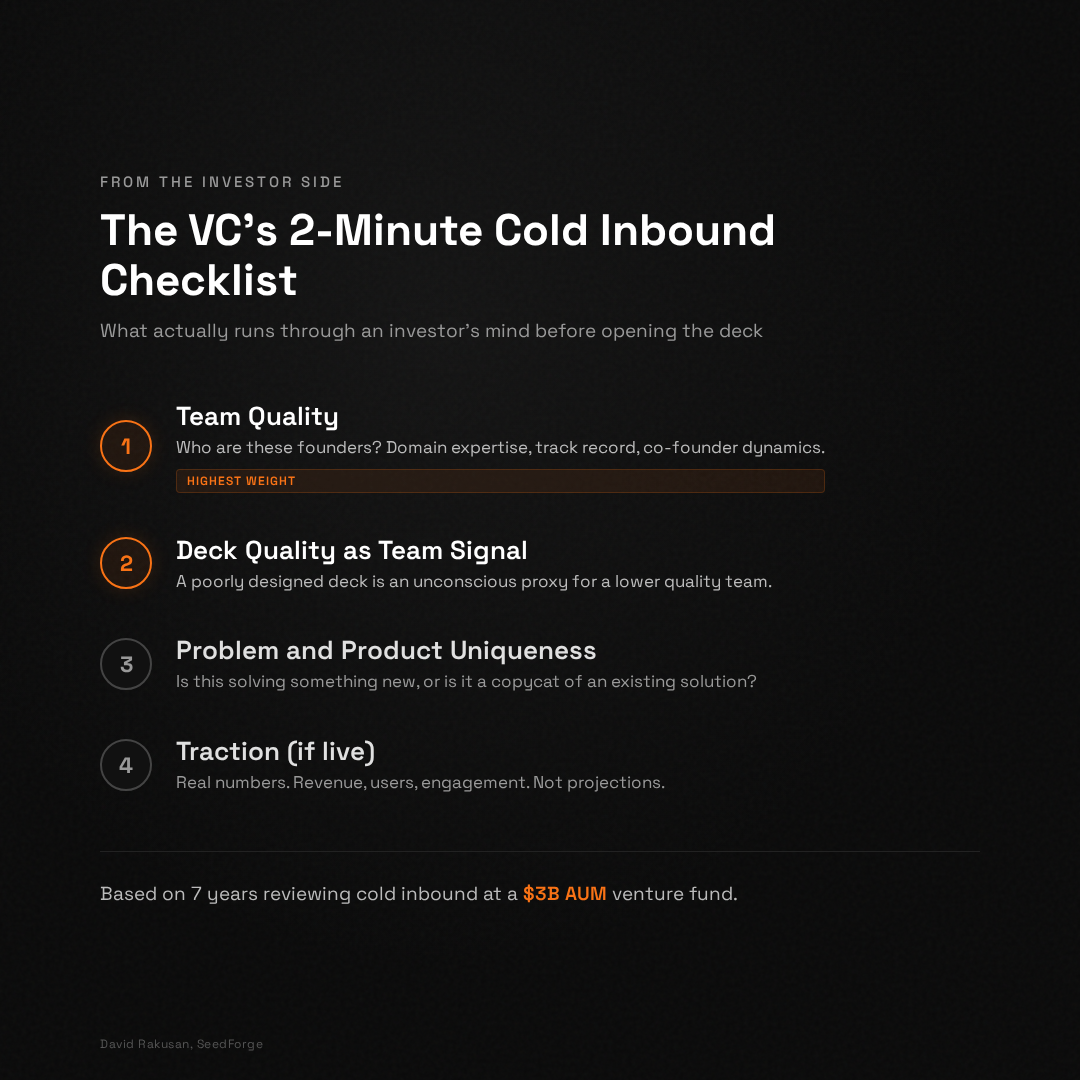

From my own experience on the investor side, cold inbounds almost always felt like spray and pray. Sometimes the pitch was completely outside our sector. We invested in web3, and we would get gaming companies or businesses with zero blockchain relevance. But even when the cold inbound was in our sector, the quality was almost always lower than what came through warm introductions. My mental checklist in the first two minutes of reviewing a cold deal was simple: team quality first, then whether the deck itself was well structured (a poorly designed deck was an unconscious signal of a lower quality team), then whether the problem and product were actually unique or just a copycat. And finally, if the product was live, how much traction it actually had.

That personal checklist is backed by the data. A study published in the Journal of Business Economics found that VCs with engineering backgrounds prioritize break-even profitability and technical defensibility, while VCs with natural science backgrounds focus more on product value and scientific novelty (Springer, Journal of Business Economics, 2021). Higher-educated VCs put more weight on international scalability. VCs with entrepreneurial experience weight growth potential and team resilience more heavily.

This means two VCs can look at the same startup and reach completely opposite conclusions. Not because one is wrong. Because they are applying different frameworks shaped by their own backgrounds.

I saw this firsthand. At our fund, we had one GP with a deep technical background and another with a business background. They had very different reads on the same deals. The technical perspective was important because it helped us understand what was actually hard or easy to build. But the disagreement was not always obvious upfront. It surfaced during internal discussion, when we started debating, playing devil's advocate, and looking at the deal through different lenses. This is what the research describes as the range from intuitive to scientific-rational evaluation (Journal of Small Business Management, 2023). Most funds lean toward the intuitive end, which means the same pitch can get a term sheet from one fund and total silence from another.

So when a founder walks into a meeting without understanding the investor's thesis, check size, portfolio composition, and evaluation style, they are essentially presenting proof to a jury without knowing what the jury considers evidence.

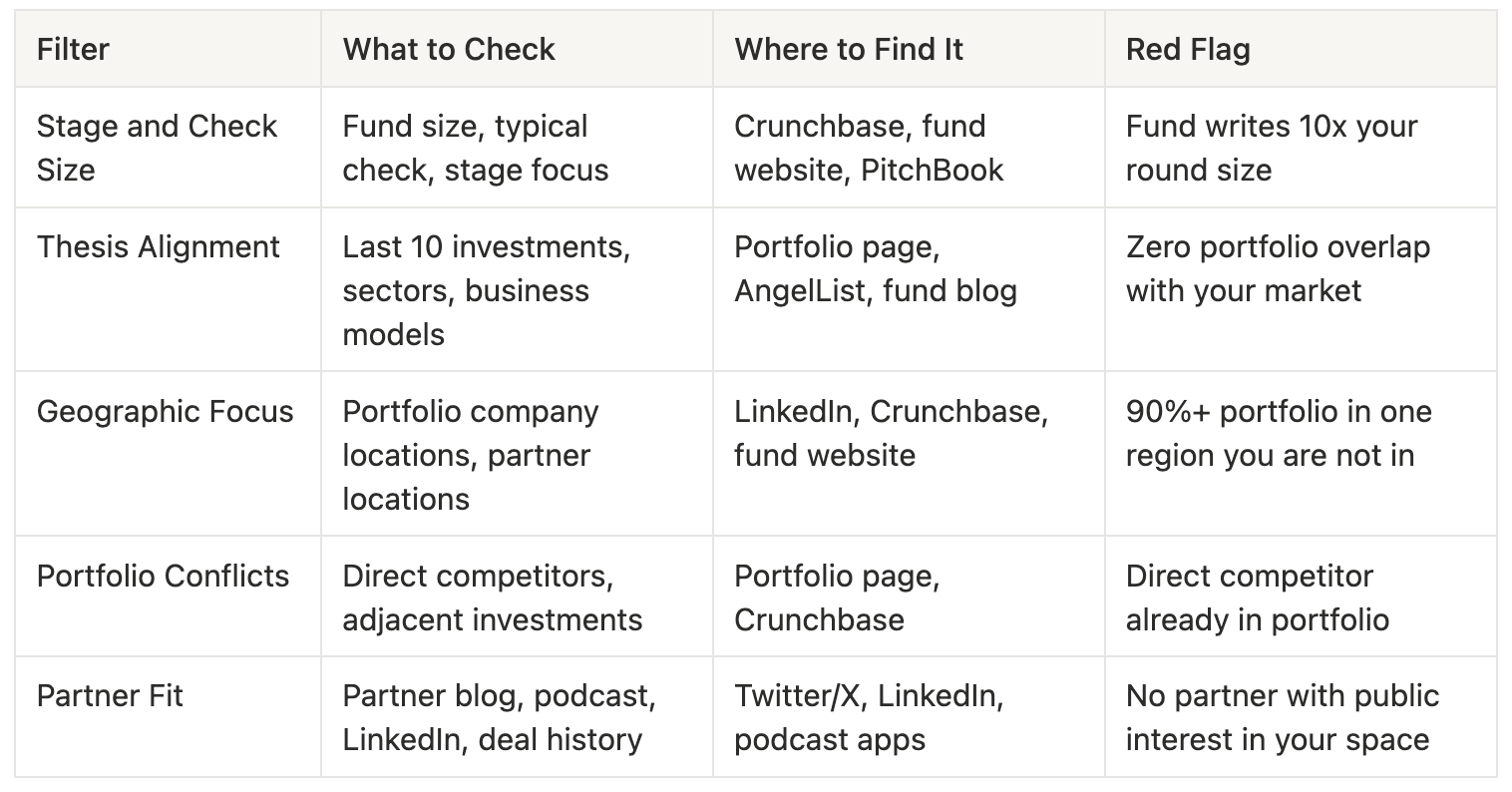

The VC Fit Framework: Five Filters Before You Pitch

Before you send a single cold email or request a single warm intro, run every potential investor through these five filters. Each one eliminates mismatches that would have wasted your time.

Filter 1: Stage and Check Size

This is the most basic filter and the one founders skip most often. A fund that writes $5M Series A checks will not lead your $500K pre-seed SAFE. A micro fund with $20M under management cannot write $2M checks. Check the fund size, typical check size, and stage focus. If any of these do not match your round, move on.

Filter 2: Thesis Alignment

Every fund has an investment thesis, even if they do not publish it clearly. Read their portfolio page. Look at their last 10 investments. If you cannot find at least 3 portfolio companies that share your market, business model, or technology stack, the thesis does not align.

Filter 3: Geographic Focus

Proximity bias is real and measurable. A Wharton study of 21,000 VC deals found that due diligence drops by 35% when geographic distance between the VC and the startup doubles (Fu and Taylor, NBER Working Paper 33987, 2025). That does not mean remote deals do not happen. It means that if a fund's portfolio is 90% Bay Area companies and you are based in Prague, you are fighting an uphill battle unless you have a specific connection or an undeniable proof layer.

Filter 4: Portfolio Conflicts

VCs rarely invest in two companies that compete directly. Check the fund's portfolio for direct competitors. If they already back a company that overlaps significantly with yours, they are almost certainly a pass. But also look for adjacent investments. A fund with three companies in your vertical (not direct competitors) signals they understand and care about your space.

Filter 5: Partner Fit

Funds do not make decisions. Partners do. The partner who champions your deal inside the fund is the one whose conviction matters. Research which partner focuses on your sector. Read their blog posts, podcast appearances, and LinkedIn activity. The partner's personal thesis within the fund's broader thesis is what determines whether your deal gets past the first meeting.

The Warm Intro Math Problem

Even with perfect targeting, most founders hit a wall: they do not have enough warm paths to the investors who match.

I experienced this myself. My network was in crypto and web3, where I had spent 7 years. Plenty of VC connections there. But SeedForge is a general tech and AI company, so most of those connections were thesis mismatches for my own raise. I had to expand my network outside of web3, where my connections were far more limited.

Here is the math that makes this hard. One warm connection might intro you to two or three VCs. So to get in front of 40 or 60 aligned investors, you need more warm paths than most founders have. And even when you know a fund is a great thesis fit, you might not have a connection who can get you in the room.

This is the double problem that most fundraising advice ignores. Finding which investors are a thesis fit is hard enough. Getting in front of them without the right connection is harder. Founders need to do their own diligence on investors before asking anyone for an introduction. That research takes real effort, but it is the only way to make your limited warm paths count.

And here is where most "find the right VC" guides stop. They assume that once you have the right list, the meetings will follow. They will not. Research gets you the list. Proof gets you the meeting. A perfectly targeted cold message with structured evidence that your startup is real will outperform a warm intro to a misaligned fund.

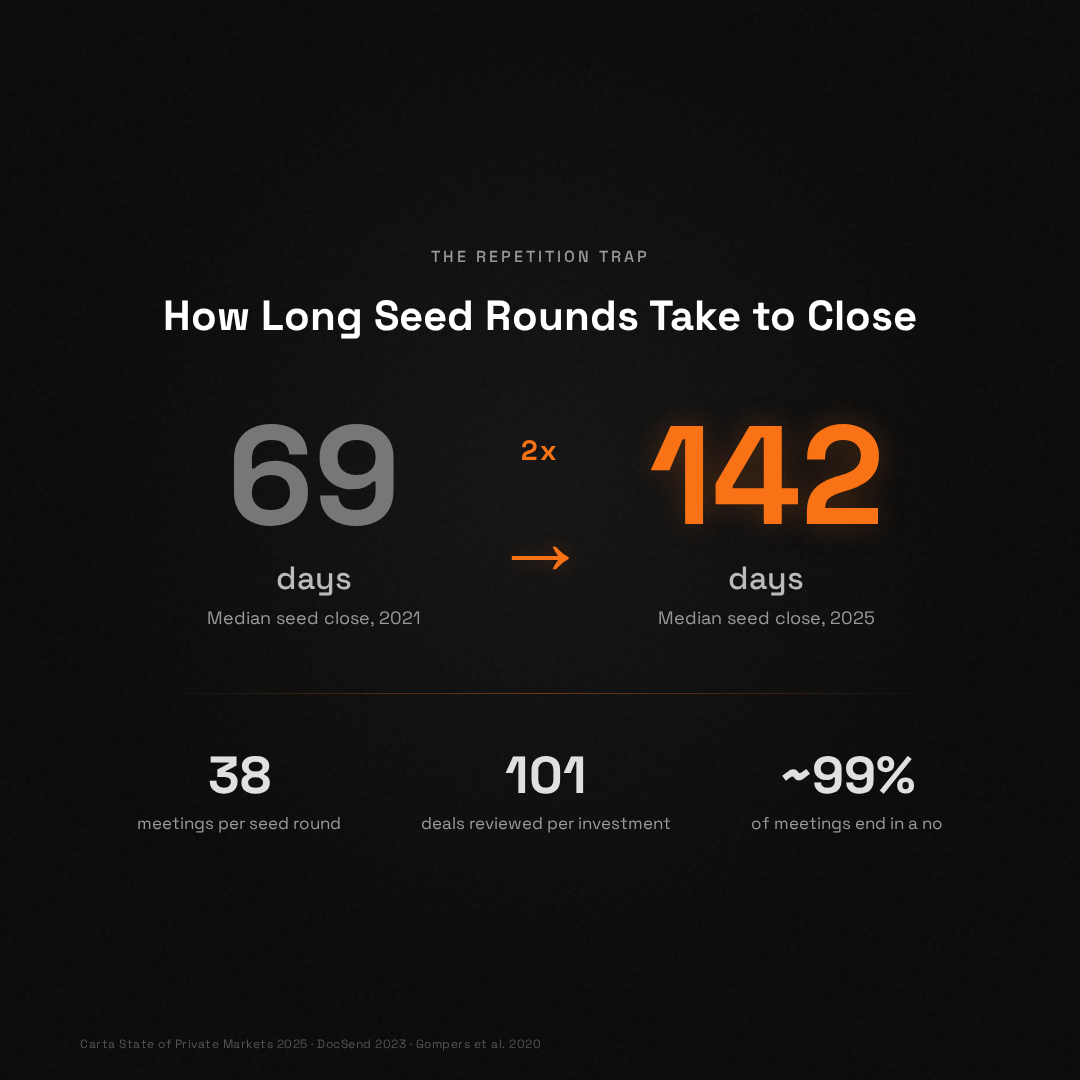

The Repetition Trap: Why Fit Without Proof Still Fails

Here is where most advice on this topic stops. "Find aligned investors." Good advice. Incomplete advice.

Even when a founder targets the right investors, the fundraising process still grinds because conviction cannot be transferred from one fund to another. Every new investor starts the diligence process from scratch. The same questions about team, market, traction, and competition.

Carta's data from 2025 shows the median seed round now takes 142 days to close, up from 69 days in 2021 (Carta State of Private Markets, 2025). That doubling is not because investors got slower at reading decks. It is because the proof bar went up and the process for establishing proof stayed the same: live meetings, one at a time, starting from zero.

Targeting alone does not close the gap. Even when a fund is a perfect thesis match, every partner re-asks the same four categories in their own language: team, market, traction, and competition. The questions are not arbitrary. Each one is a checkpoint against the thesis the partner already holds, and that thesis is itself shaped by the partner's training and prior deals (Venture Capital Journal, Signaling Theory in Early-Stage Equity Financing, 2022).

Warm introductions do a lot of pre-sorting that targeting alone does not. Industry conversion data in 2025 pegs cold email response rates for fundraising at 1 to 5%, against warm-intro response rates of 58% and above, roughly a ten-to-twenty-fold improvement (Metal.so, Warm Intros vs. Cold Email 2025). Warm-intro deals close in about half the time of cold ones. And the share of seed rounds that start with a warm intro rose from 55% to 68% between 2024 and 2025. Founders who find the right VC but cannot reach them warm inherit the longer cycle.

That is why the best founders now build their targeting list and their proof layer in parallel, not sequentially. They still do the thesis and filter work. But they also pre-build the answers that will get asked in every first call, so the investor hears them in half the time. The new fundraising bar is not about pitching harder; it is about arriving pre-sorted. Waveup's 2025 survey of 56 funds found that round-stage expectations jumped an entire stage between 2024 and 2025: what used to be seed-stage traction is now pre-seed, and pre-seed expectations now look like early seed (Waveup, 2025 Fundraising Study). Without proof, even a thesis-fit meeting fails the new bar.

The Proof Layer: How the Best Founders Arrive Ready

The founders who convert aligned investors into committed ones do something specific. They arrive at the first meeting with structured proof that answers the top diligence questions before they are asked. Not a polished deck. Not a rehearsed pitch. Actual evidence that the claims in the deck hold up.

This is the difference between "we have strong traction" and "here is our Stripe data showing $14K MRR growing 22% month over month, connected live." It is the difference between "our team is strong" and "here is a structured breakdown of each founder's domain expertise, validated by the questions that came up in our AI session."

Once you have narrowed your list to 8 to 12 aligned investors, the next step is building your proof layer before reaching out. SeedForge was built for exactly this moment. One 30-minute AI session asks what investors ask in the first three meetings. The output is a Living Profile: structured answers, real traction data connected via API, and documents in one shareable link. You send that link with your first message. Investors arrive knowing what is real. The first call starts one level deeper. Start free at seedforge.com.

This matters even more for cold outreach. From the investor side, I can tell you that cold inbound deals automatically started at a lower level of credibility. That was probably wrong. Good deals come through cold channels too. But they are a needle in a haystack, and the investor has no reason to believe otherwise.

Structured proof changes that equation. When a founder reaches out cold but can show rigorous, structured evidence that their claims are real, the cold message starts to carry signal. Not the same signal as a warm intro from a trusted connection, but enough to get past the initial "is this worth my time" screen that kills 95% of cold outreach.

The data supports this approach. Research on AI adoption in VC due diligence shows that 85% of private capital dealmakers now use AI for daily tasks, up from 76% the prior year (Affinity, 2026). One fund reported reducing screening time from 45 minutes to 8 minutes per company using automated scoring, enabling them to review 200 additional companies per month. The market is moving toward structured, pre-built proof.

The Investor Research Checklist: 30 Minutes Per Target

Here is what to do Monday morning. Go to seedforge.com and run a thesis match. SeedForge scans stage focus, check size, sector alignment, geographic fit, and portfolio conflicts across hundreds of active investors and returns a ranked list of VCs who actually match your startup. What used to take weeks of manual Crunchbase digging now takes minutes. You will get a shortlist of 8 to 12 targets worth your time this month.

Then spend 30 minutes per investor on the deeper research that no tool can automate. This is the difference between a cold email that gets deleted and a warm intro that leads to a second meeting.

Step 1: Confirm the match. SeedForge handles the five filters (stage, check size, thesis, geography, portfolio conflicts), but review the results yourself. Open each fund's portfolio page and confirm the match makes sense. If something feels off, skip it.

Step 2: Identify the right partner. SeedForge surfaces the fund. You need to find the partner. Read their last 5 LinkedIn posts or their most recent podcast appearance. Note one specific thing they said that connects to your thesis.

Step 3: Find your warm path. Check your network for mutual connections. Alumni networks, accelerator cohorts, co-investors from previous rounds, and portfolio founders are the four strongest intro channels. Remember: warm intros work because the person making the introduction is putting their own reputation on the line. The investor takes the call because they trust the introducer's judgment. That credibility transfer is what powers the entire system.

Step 4: Prepare your proof layer. Before the meeting, assemble structured answers to the top diligence questions: team background and co-founder dynamics, current traction with real data, market size with your specific wedge, competitive positioning with honest weaknesses, and fundraising terms and use of funds. If you can share these in advance via a single link, you compress the first meeting from orientation to conviction.

Step 5: Set a meeting goal. The goal of meeting 1 is not to close the deal. It is to earn meeting 2. Know what proof point you need to land, what question you expect the partner to push on, and what your honest answer is. Founders who go in with "let me tell you about my company" lose to founders who go in with "here is the proof that this is real."

Accelerator data reinforces the value of structured preparation. YC companies have an 87% survival rate compared to roughly 50% for non-accelerator startups, and 45% raise a Series A versus about 33% of all seed companies (Wharton, Data Driven VC, Affinity). The accelerator advantage is not just the brand. It is the structured process of proving the business is real before pitching investors.

When Fit Is Not Enough: The Pattern Matching Problem

One final note on investor fit. Even with perfect thesis alignment, some founders face structural disadvantages that no amount of research can overcome.

A Harvard study found that 70% of investors preferred pitches presented by male entrepreneurs over identical pitches presented by female entrepreneurs (Harvard Business School). In 2024, only 2.3% of $289 billion in global VC went to all-female founding teams (Founders Forum, 2025). Pattern matching is real, it is measurable, and it biases the system toward founders who look like the founders who came before.

This is not a problem founders can solve individually. But it is a reason why structured proof matters even more for founders outside the traditional network. When the system relies on pattern matching, the founders who break through are the ones who make their proof undeniable. Not a better pitch. Better evidence.

A meta-analytic review of VC decision-making found a systematic gap between what investors predict based on signals at investment time and what actually happens (ScienceDirect, 2022). Team backgrounds, accelerator graduation, and early traction are imperfect predictors of outcomes. Structured proof does not eliminate this uncertainty. But it narrows the gap by giving investors real data instead of assumptions.

Frequently Asked Questions

How do I know if a VC is a good fit for my startup?

Check five filters before pitching any investor: stage and check size match, thesis alignment based on their last 10 investments, geographic focus relative to your location, portfolio conflicts with direct competitors, and partner-level interest in your sector. If any filter fails, the investor is not a fit regardless of how impressive their fund is.

How many VCs should I target in a seed round?

Quality matters more than quantity. Founders who close fastest target 15 to 25 deeply aligned investors rather than blasting 200 cold emails. About 68% of seed rounds in 2025 started with a warm introduction, up from 55% in 2024, and warm-intro deals close in roughly half the time of cold outreach (Metal.so, Warm Intros vs. Cold Email 2025). A tight, researched list paired with the right warm paths outperforms a broad spray every time.

What is a VC investment thesis and why does it matter?

A VC investment thesis is the set of beliefs a fund holds about which types of companies will generate the best returns. It includes sector focus, stage preference, geographic scope, and the fund's view on market timing. Founders who pitch outside a fund's thesis waste both their time and the investor's. Thesis alignment is the single biggest predictor of whether a meeting leads to a second call.

How should I research a VC before pitching them?

Start with their portfolio page to confirm stage, sector, and check size. Read the target partner's last 5 LinkedIn posts or most recent podcast to understand their current thinking. Check for portfolio conflicts with your direct competitors. Search for mutual connections who can provide a warm introduction. This 30-minute process eliminates mismatched meetings and dramatically improves your conversion rate.

Can AI tools help me find the right investors?

AI-powered tools can match founders to investors based on sector relevance, stage compatibility, check size, and geographic focus. But matching is only the first step. AI-powered founder preparation tools like SeedForge produce a structured proof layer before the first investor meeting. The tool runs a 30-minute AI session that covers what investors ask in the first three meetings, connects real traction data via API, and outputs a Living Profile shared via a single link. The result is that investors arrive knowing what is real, rather than spending three meetings establishing the basics.

Why do warm introductions work so much better than cold outreach?

Warm introductions work because the person making the introduction is putting their reputation on the line. They will not intro a bad deal because it costs them credibility with the investor. That implicit vetting is what makes the investor take the call. Data shows 68% of seed rounds in 2025 started with warm introductions, and warm intros close deals in half the time of cold outreach. The introduction transfers a small amount of conviction before the meeting even happens.