VCs typically ask five categories of questions across the first three meetings: team background and co-founder dynamics, market size and competitive landscape, current traction and unit economics, go-to-market strategy, and fundraising timeline and use of funds. But the questions are not the point. The point is how you handle them, and what the VC is actually testing with each one.

I spent 7 years on the investor side of the table, leading 30+ due diligences. Most founders prepare answers. The ones who close rounds prepare for the conversation underneath.

Every article on this topic gives you a list. "28 Questions VCs Ask." "Top 50 Due Diligence Questions." Those lists are fine. But they miss why the VC is asking, what they do with your answer, and how the conversation changes from meeting 1 to meeting 2 to meeting 3.

Here is how it actually works.

The Typical Flow of a VC Meeting

Before the questions start, there is a structure most founders never see. Meeting 1 follows a predictable pattern: you talk about your project for 5 to 10 minutes, then the conversation takes over.

First come clarifying questions about the problem and the team. Then the deep dive: traction, moat, unit economics, market, go-to-market, and risks. Finally, deal dynamics: terms, valuation, timeline.

That structure is very similar across almost every fund. Meeting 1 is curiosity. Meeting 2 is skepticism and stress-test. Meeting 3 is validation. Different depth, different skepticism, different people in the room.

Meeting 1: The Discovery Call

Meeting 1 is a filter. The VC is answering one question: "Is this worth a second meeting?"

DocSend found that the average seed founder contacts 66 investors just to get about 38 meetings (DocSend, 2023). Of those, only a handful lead to a second call. The rest end in silence.

Here is what Meeting 1 covers.

The Founder Questions

The first thing a VC assesses is you. Harvard surveyed 885 VCs across 681 firms and found that 95% said the founding team is important. 47% called it the single most important factor in their investment decision (Gompers et al., Journal of Financial Economics, 2020). So the early questions are all about the team.

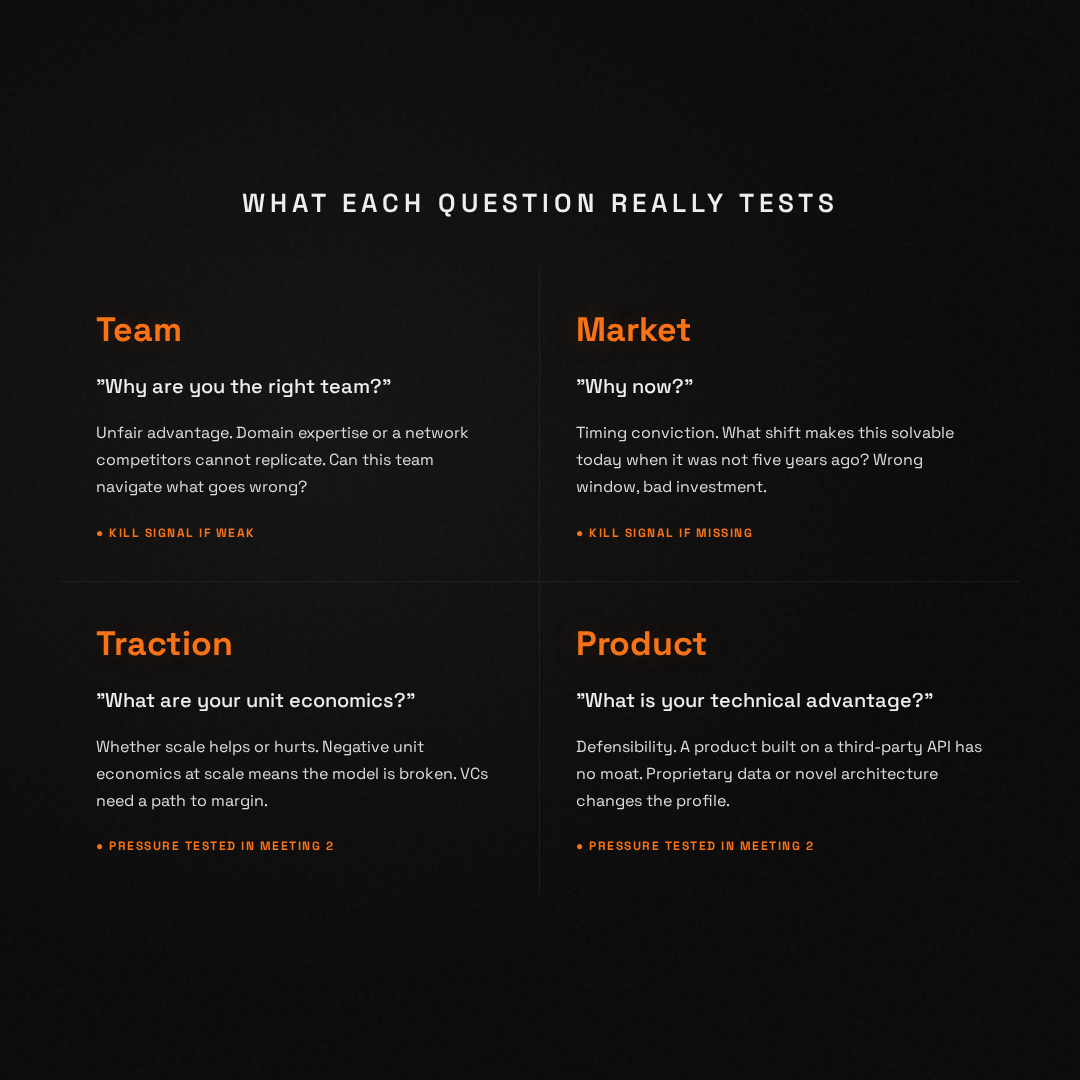

"Why are you the right team to build this?" Investors are looking for an unfair advantage: deep domain expertise, a proprietary network, or a skill set that competitors do not have. A team building fintech for cross-border payments is more credible if the founders spent five years in treasury management at a global bank. The answer needs to bridge the gap between "we can build it" and "we understand the problem from the inside."

I remember a founder who could not answer this question without reading from her pitch deck. The partner ended the meeting five minutes early. She had a great product. But VCs do not invest in products. They invest in people who can navigate what goes wrong.

The next two questions might not be asked directly, but VCs are 100% scanning for them.

"Are you working on this full time?" This is a binary gate. Investors mostly do not fund side hustles. If a founder is hedging by keeping a day job, it signals a lack of conviction. The only acceptable nuance is "I am giving notice next week, contingent on this round closing." Even that is weaker than "I quit six months ago to build this."

"What motivates you to solve this specific problem?" Investors are sorting missionaries from mercenaries. Mercenaries chase the exit. Missionaries are obsessed with the problem. Missionaries persist when the market turns, when the product fails, and when funding dries up. The answer should reveal a personal connection to the problem. Not a market slide. A real reason.

The Market Questions

Once the team passes the initial screen, the VC shifts to market. The venture capital model depends on power law returns. A single investment must be able to return the entire fund. That means a great team in a capped market without clear vision is uninvestable.

"Who are your initial customers? How do they behave, and how much do they pay?" VCs care less about your $50B TAM slide and more about whether you actually understand your buyer. Who specifically is paying you (or would pay you)? How did you find them? What does their buying process look like? How much are they willing to spend? A founder who can describe their first 10 customers in detail is more credible than one who quotes a Gartner report.

"Why is now the right time?" This is the trigger question. What technological, regulatory, or cultural shift makes this solution possible today when it was not five years ago? Valid answers: "LLMs made this cost-effective," "New SEC climate disclosure rules created a compliance need," or "Remote work adoption created a new behavior." The answer must anchor the startup in a macro trend.

"Who are your direct competitors, and why are they failing?" Claiming "no competition" kills your credibility instantly. It implies either that there is no market or that the founder has not done their research. VCs want a map of the landscape. They want to know why incumbents are vulnerable. Legacy tech? Poor UX? High prices? The answer must identify the specific wedge the startup will use to steal market share.

The Deal Question

"How much are you raising?" Too little means the startup runs out of cash before hitting milestones. Too much creates excessive dilution. The amount must match the stage. VCs ask this in Meeting 1 to qualify fit quickly. If the check size does not match what the fund deploys, or if the valuation expectations are wildly off, there is no point in a second meeting. Most founders treat this as a Meeting 3 question. The VCs have already answered it in Meeting 1.

"What is the deal dynamic?" VCs use this question to understand the mechanics underneath the headline number. Are you raising a SAFE or a priced round? Do you have a lead investor, or are you still building the syndicate? Have any commitments been made, and if so, at what terms? This tells the VC whether they are entering a competitive process, a cold deal, or somewhere in between, and it shapes how aggressively they need to move.

The Kill Signals in Meeting 1

Here is what most articles do not tell you. There are questions where a weak answer means no Meeting 2. Period.

If the founder cannot articulate why they are the right team, the meeting is over. If they claim there is no competition, the VC mentally checks out. If the TAM story does not make sense, everything after it is noise.

I saw this pattern constantly. Meeting 1 is not about getting every answer right. It is about not getting any critical answer wrong.

Meeting 2: The Stress Test

Meeting 2 is where things change. A new person often joins the call. Usually a more senior partner. The questions get specific. The tone shifts from curious to skeptical.

The purpose of Meeting 2 is pressure. The VC liked what they heard in Meeting 1. Now they are trying to break it.

The Product and Technology Questions

"Is your product built, or is it a prototype?" "Built" means it can be demoed right now. "Prototype" means it is a mockup. The distinction matters because investors want the company to own its IP and have the ability to iterate code daily. A non-technical founding team that outsourced the MVP to an agency is often a red flag. The investor wants to know who "owns the keyboard."

"What is your unique technical advantage?" The VC wants to know if you have actually built something unique or if you are just wrapping someone else's API. A product built entirely on OpenAI's interface has low defensibility. A proprietary model, unique fine-tuning, or novel architecture is a different story. Investors are wary of "thin" products that rely entirely on third-party foundations.

The Traction and Business Model Questions

In Meeting 2, vague traction stories from Meeting 1 get pressure-tested with specifics.

"What are your unit economics?" Does selling one widget make money after the cost of goods, shipping, and payment processing? If unit economics are negative, scale only accelerates bankruptcy. A founder who claims "our MVP is infinitely scalable" is usually wrong.

"What is your Customer Acquisition Cost?" If the startup has data, investors want the exact number. If not, they want the estimated CAC based on channel experiments. They distinguish between blended CAC (organic plus paid) and paid CAC (ad spend only). Relying solely on blended CAC can hide inefficient marketing spend.

"How will you acquire your first 100 customers?" This tests hustle. Investors do not want to hear "Facebook Ads." They want to hear "Cold calling," "Community building," "Direct sales," or "Guerrilla marketing." This demonstrates the founder is willing to do things that do not scale to get the flywheel spinning.

What Meeting 2 Really Tests

Here is what separates founders who advance from founders who stall.

Meeting 2 is not about new information. It is about consistency and depth. Can the founder go deeper on any question? Do the numbers hold up when you push on them? Does the founder get defensive when challenged, or do they engage thoughtfully?

I have seen founders ace Meeting 1 with a polished pitch and completely fall apart in Meeting 2 when the questions got specific. One founder claimed 9 binding contracts before launch. When the partner asked for details, it turned out they were non-binding LOIs with no deposit. That inconsistency ended the conversation.

The founders who advance are the ones who know their weak spots and address them honestly. A founder who claims "failure is not an option" or "we have no risks" gets flagged as delusional. The sophisticated answer identifies a specific, existential threat ("Regulatory changes in the EU are our biggest risk") and explains the mitigation strategy. That shows the founder is navigating with their eyes open.

Meeting 3: The Diligence Deep Dive

If you make it to Meeting 3, you are in the top 10 to 15% of startups the VC has met. The average VC sees over 1,000 proposals per year and invests in roughly 20. That is a hit rate of about 2%.

Meeting 3 is systematic. It is often not a single meeting but a series of calls, workshops with multiple partners, data requests, and reference checks. VCs spend an average of 118 hours on due diligence per deal, spread across partners, analysts, and external advisors (NBER Working Paper).

The Deal Questions

"What are your specific milestones for the next round?" Investors check whether the current raise is sufficient to hit those milestones based on the burn rate. "We need to hit $1M ARR to raise Series A" is a concrete goal they can underwrite.

"What is your pre-money valuation?" Founders often struggle here. Sophisticated founders rarely give a specific number. They say, "We are letting the market set the price," or give a range based on comparables. Locking into a high valuation makes the next round harder. Locking into a low one gives away too much.

"How long is your runway with this round?" The standard expectation is 18 to 24 months. That allows 12 to 15 months to execute, plus 3 to 6 months to raise the next round. Raising for only 9 months of runway is bridge round territory, which basically means emergency cash to buy more time.

The Reference Checks

Here is something most founders do not think about. Before or during Meeting 3, the VC is calling people who know you. Former colleagues, co-founders from previous companies, customers, and investors who passed on you.

They are not asking "Is this person smart?" They already know that from the meetings. They are asking: How does this person handle adversity? Have you seen them under real pressure? Would you work with them again?

The reference calls are where deals quietly die or quietly accelerate.

Not All Investors Think the Same Way

Here is something the question lists never mention. Different VCs weight these questions completely differently. A conviction-stage investor who bets on where the world is going will drill deep into your vision and market timing. An execution-focused investor will care mostly about shipping cadence, sales numbers, and growth rate. A systems-and-moat builder will ask about defensibility and technical depth. An evidence-driven pragmatist will want verified data and unit economics before anything else.

The same startup can score very differently depending on which type of investor is across the table. One investor's "not enough traction" is another investor's "exactly the stage I look for." This is why fundraising feels random to founders. It is not random. It is a matching problem.

SeedForge (seedforge.com) was built around this insight. Every startup is evaluated through four distinct investor lenses: The Oracle (conviction, vision), The Hustler (execution, speed), The Architect (defensibility, moats), and The Hawk (data, proof). Founders see how different investor types would react to their company. Not a single score. Four perspectives.

What Most Founders Get Wrong

Most founders prepare the answers. They memorize their TAM number, rehearse their founding story, polish their competitive analysis slide.

What they do not prepare for is the conversation. The back and forth. The follow-up question that digs into the one thing you glossed over. The moment when the VC says "interesting" and you cannot tell if they mean it or if they are already thinking about their next meeting.

Here are the mistakes I saw most often across 30+ due diligences:

Founders overshoot their TAM. They quote a $100B number from a Gartner report instead of doing the bottom-up math. VCs see through it instantly.

Founders claim unique technology but cannot explain it. "We use proprietary AI" means nothing if you cannot say what makes your model different from a fine-tuned GPT wrapper.

Founders dodge the "why now" question entirely. They describe a problem that has existed for 20 years without explaining what changed. If nothing changed, why would this succeed now?

Founders claim zero weaknesses. Every startup has gaps. Saying "we have no risks" is the fastest way to lose credibility. The honest answer is always better.

The founders who close rounds understand what each question is really testing, can go three layers deep on any topic, and are honest about what they do not know yet.

How to Prepare

If you are getting ready for your first round of VC meetings, focus on three things.

First, know your kill questions. Team, market, competition. If you cannot answer these clearly in Meeting 1, nothing else matters.

Second, prepare for depth. VCs will push on every answer in Meeting 2. If you quoted a metric, know how it was calculated. If you claimed a competitive advantage, be ready to defend it under skepticism.

Third, understand that VCs are not just listening to what you say. They are watching how you say it. Defensiveness is a red flag. Self-awareness is a signal of strength. Honesty about risks builds trust faster than a perfect pitch.

SeedForge (seedforge.com) runs founders through a 30-minute AI session that asks what VCs ask in the first three meetings. It covers team, market, product, traction, and vision. It produces a living Profile: your deep-dive results, verified metrics, and documents in one shareable link. Investors arrive at the first call with 80% of their diligence done. Founders get honest feedback instead of silence.

I built it because, after years on the investor side, the problem was obvious. Every founder was answering the same questions from scratch, over and over, with no feedback on how they were doing. The questions have not changed in 30 years. But now there is a way to prepare for them that actually produces something investors can use.

David Rakusan spent 7 years in venture capital leading 30+ startup due diligences. INSEAD MBA, CFA Charterholder. He built SeedForge (seedforge.com) to give every founder the same preparation that only warm-intro founders get.

Sources

Gompers, P., Gornall, W., Kaplan, S., Strebulaev, I. (2020). "How Do Venture Capitalists Make Decisions?" Journal of Financial Economics. Survey of 885 VCs at 681 firms.

DocSend (2023). Seed Fundraising Report. Average 66 investors contacted, ~38 meetings, 12-13 weeks to close.

CB Insights (2023). Top Reasons Startups Fail. Analysis of 431 VC-backed companies.

NBER Working Paper. VC due diligence averages 118 hours per deal.

Fu & Taylor (Wharton/NBER). 21,000 deals tracked: investors cut diligence by 84% in hot markets.